The Corporate Sustainability Due Diligence Directive (CSDDD) and the Corporate Sustainability Reporting Directive (CSRD) are new EU sustainability legislations with a lot in common — not just in name. Here’s a breakdown of key similarities and differences to help you skip the acronym headache.

What are CSDDD and CSRD?

CSDDD is a due diligence legislation requiring companies to identify, prevent, reduce and end negative human rights and environmental impacts in their operations and value chains. Companies also need to report annually on impacts and actions. Read our blog on everything you need to know about CSDDD.

CSRD is a reporting directive requiring companies to perform a double materiality assessment and produce an annual report disclosing the impacts, risks, opportunities and action plans associated with their material environmental, social and governance (ESG) issues.

What are the key similarities and differences between CSDDD and CSRD?

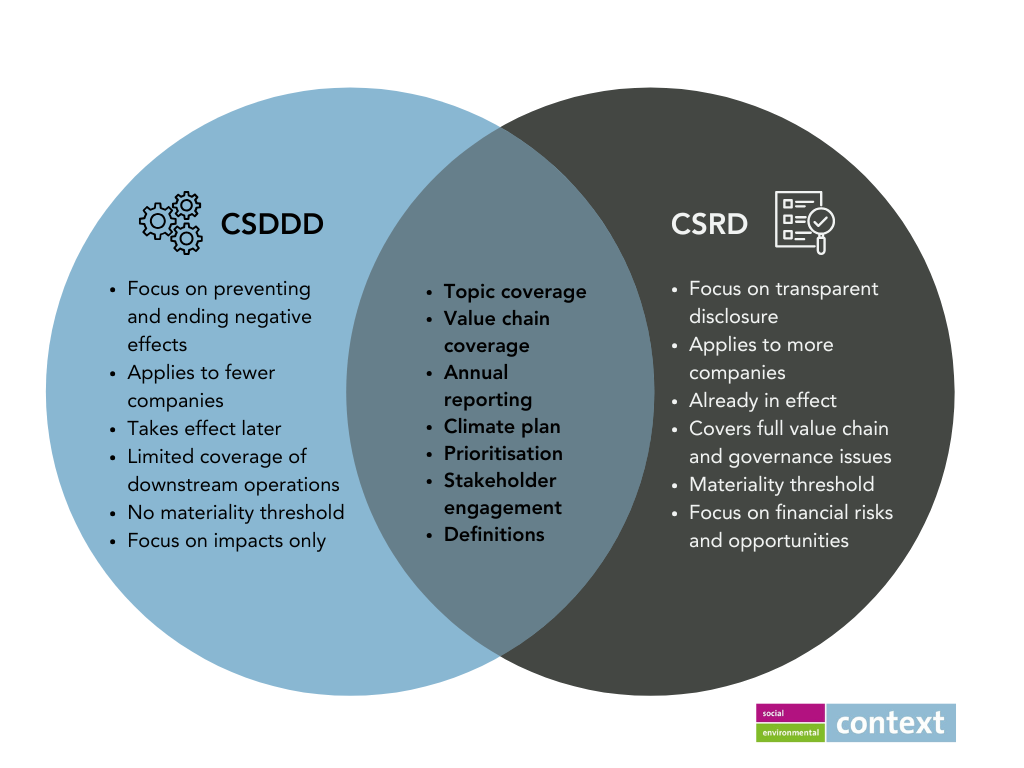

- Core focus

CSDDD focuses on doing — taking action to end adverse impacts. CSRD focuses on materiality and reporting — identifying and transparently disclosing impacts. But there is crossover. Like CSRD, CSDDD also requires annual reporting on adverse impacts and mitigation actions. And although CSRD is more focused on reporting than action, it does ask companies to disclose their climate plans in line with limiting global warming to 1.5°C.

- Scope and timeline

Both apply to large companies operating in the EU. CSRD applies to more companies, including EU-listed SMEs, and is already in effect. CSDDD is narrower — only large companies with 1,000+ employees and a net turnover of €450+ million are in scope. Companies must comply with CSDDD by 2027 at the earliest.

- Topic coverage

The topics covered by the legislations are broadly aligned. Both include human rights and environmental impacts and acknowledge their deeply interconnected nature. CSRD has the bigger picture in mind, covering issues related to governance, consumers and end-users. It also focuses on financial risks and opportunities, unlike CSDDD.

- Value chain coverage

Both cover companies’ own operations as well as upstream and downstream operations — inside and outside Europe. But CSDDD has a smaller downstream scope, only covering certain operations such as distribution, transport and storage. CSRD goes further and covers end-users and product disposal.

- Climate plans and reporting

Both ask for a climate transition plan aligned with limiting global warming to 1.5°C, and a publicly available annual report covering impacts and actions. CSRD’s reporting scope is more ambitious — see topic coverage above.

- Prioritisation

Both require companies to prioritise impacts based on severity and likelihood. But CSRD’s double materiality assessment means companies don’t have to report on issues that are less relevant to them. CSDDD still requires companies to address lower priority impacts after addressing their higher priority issues.

- Stakeholder engagement

Organisations need to continuously engage with internal and external stakeholders for both legislations. CSRD adopters must engage with stakeholders to perform the double materiality assessment and gather the necessary data. CSDDD requires stakeholder engagement throughout the due diligence process — from strategy-setting and training to providing a complaints procedure and monitoring due diligence measures.

- Targeted SME support

Unlike CSRD, CSDDD adopters must try to avoid overly burdening business partners who are small and medium-sized enterprise (SMEs). This could include offering training to SME suppliers or upgrading management systems, and where necessary providing financial support.

- Definitions

The definitions of impacts, risks and opportunities are aligned across the legislations. Impacts refer to potential and actual effects organisations have on the environment and society. Risks and opportunities refer to how sustainability issues could affect the organisation’s balance sheet.

What’s left to do if you already report to CSRD?

If you’re already on top of CSRD then you’re covered for CSDDD reporting and climate plan requirements. But there are some due diligence measures you’ll still need to carry out for CSDDD:

- Create a policy that ensures risk-based due diligence.

- Carry out in-depth assessments of individual suppliers in prioritised areas.

- Take measures to prevent and mitigate potential adverse impacts, and minimise and end actual adverse impacts.

- Provide a notification channel and complaints procedure.

- Monitor the effectiveness of due diligence measures and update them accordingly.

- Provide targeted and proportionate support for business partners who are SMEs, including non-discriminatory contractual assurances.

Context is ready to support you with all your CSRD and CSDDD needs — from devising strategies and conducting double materiality assessments, to writing policies and reports. If you would like to talk about your organisation’s needs, please get in touch via www.contextsustainability.com or helen.fisher@contexteurope.com.