The sustainability universe is watching as the EU’s new mandatory sustainability reporting standards go through the wringer. Meanwhile, the International Sustainability Standards Board (ISSB) Standards are gaining momentum.

The ISSB, born at the 2021 UN climate conference, COP26, is responsible for building a framework for companies everywhere to report sustainability information in a consistent way. Already, 17 jurisdictions across the globe — including Australia, Brazil, Hong Kong, Mexico and Nigeria — have confirmed full or partial adoption of the ISSB’s standards. An additional 16 — including Canada, China, Japan, Singapore, Uganda and the UK — are in the process of formally adopting the framework to some degree. This group of 33 committed countries includes 11 of the world’s 20 largest economies.

With the ISSB Standards picking up steam, you may be wondering what you need to know (perhaps while internally panicking at the thought of yet another sustainability reporting framework). To help get you started, here are five ISSB FAQs answered.

1. What is the purpose of the ISSB Standards?

Companies globally are increasingly expected and mandated to share sustainability information. Why? To give people who want to know about a company (e.g. customers, investors, employees, partners, rating and ranking organisations, etc.) a complete picture of its performance, progress, prospects and plans.

But there is currently no one framework telling companies which sustainability information to report. Rather, there are many frameworks asking for different types of qualitative and quantitative information. This means we’re often reading cherry-picked success stories and comparing apples with oranges when evaluating sustainability performance across companies.

The ISSB Standards aim to change this. They were developed in response to strong market demand for a global sustainability reporting baseline to give companies clear guidance on what to report. In the way that traditional financial reporting is consistent and comparable across the world thanks to common standards, the ISSB wants sustainability reporting to be the same.

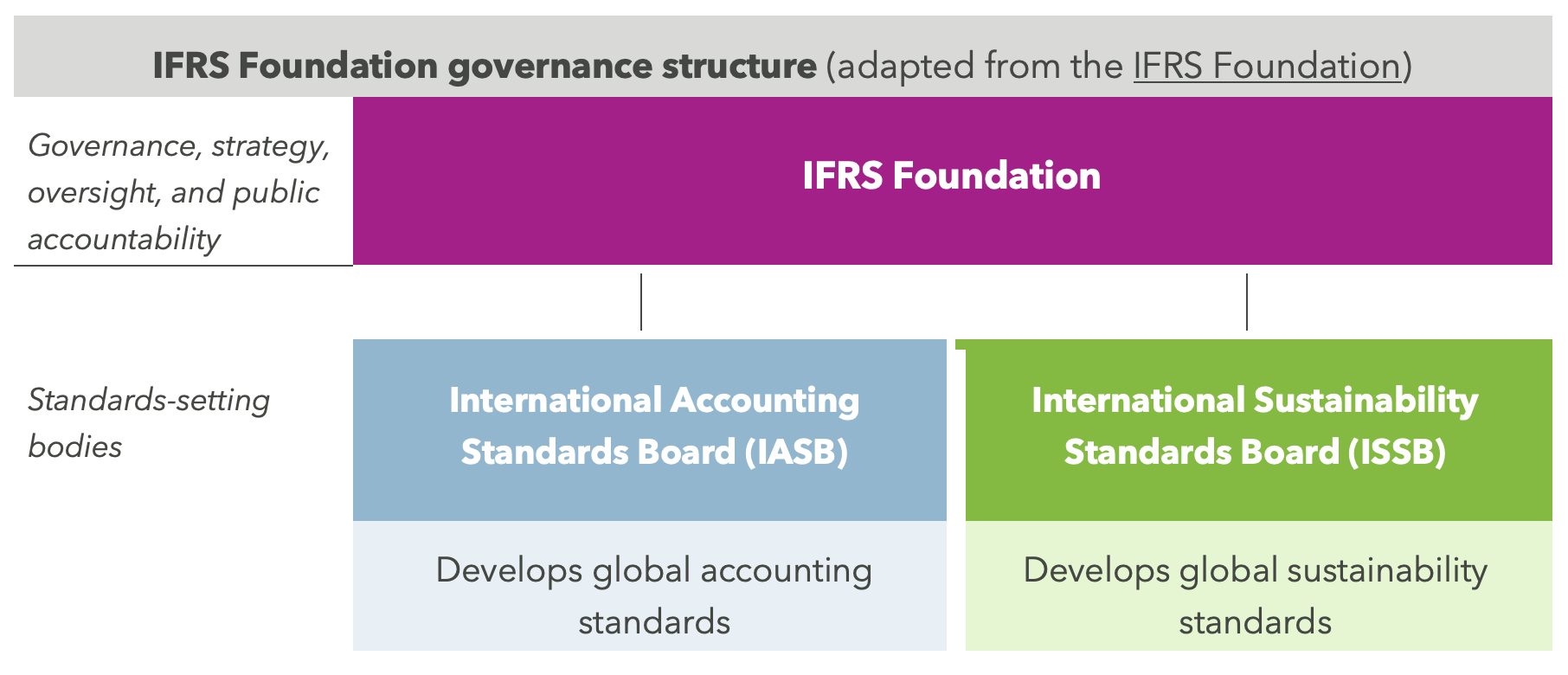

2. Who develops and oversees the ISSB Standards?

The International Financial Reporting Standards (IFRS) Foundation establishes the common global framework for financial reporting through the International Accounting Standards Board (IASB), its standards-setting body. In 2021, the IFRS Foundation introduced the ISSB — a new branch in charge of developing an equivalent international framework for sustainability reporting.

In the interest of developing a single global standard, several big sustainability frameworks and organisations were essentially absorbed into the IFRS Foundation — including the Climate Disclosure Standards Board (CDSB), the Task Force for Climate-related Financial Disclosures (TCFD), the Value Reporting Foundation’s Integrated Reporting Framework, the Sustainability Accounting Standards Board (SASB) Standards, and the World Economic Forum (WEF)’s Stakeholder Capitalism Metrics.

3. What types of information do companies need to report under the ISSB Standards?

The ISSB Standards are designed to provide useful sustainability information to external stakeholders who make financial decisions about a company (investors, lenders and creditors). So, they focus disclosures on sustainability-related risks and opportunities that could impact the decisions these stakeholders make. In other words, they focus on financial materiality.

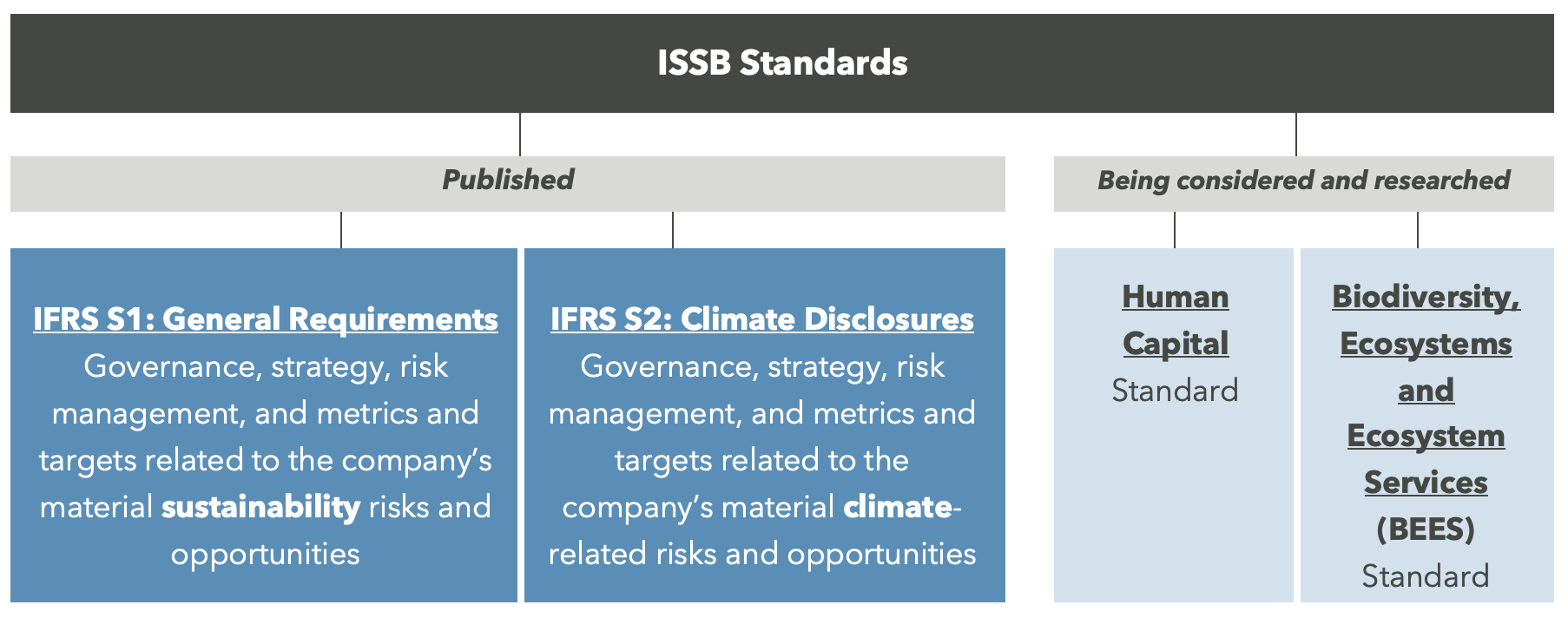

There are two active ISSB Standards — including general disclosures (IFRS S1) and specific climate disclosures (IFRS S2) — with others being explored. Both active standards ask for information on governance, strategy, risk management, and metrics and targets for financially material sustainability topics. This mirrors the structure of the TCFD recommendations, today’s most widely adopted recommendations for climate-related risk and opportunity disclosures — since absorbed into the IFRS Foundation.

4. What is the difference between the ISSB Standards and other common reporting frameworks?

While the ISSB Standards aim to be the global baseline for sustainability reporting, they currently exist in a busy space. The European Sustainability Reporting Standards and the Global Reporting Initiative Standards are the two other big players. The fundamentals that set them apart are their breadth of focus and approach to materiality, though there is a level of interoperability across all three.

| International Sustainability Standards Board (ISSB) Standards | European Sustainability Reporting Standards (ESRS) | Global Reporting Initiative (GRI) Standards | |

| First launched | 2023 | 2023 | 2000 |

| Standard developers | International Sustainability Standards Board (ISSB) | European Financial Reporting Advisory Group (EFRAG) | Global Sustainability Standards Board (GSSB) |

| Geographic focus | Global | EU | Global |

| Key audience(s) | 🎯 Focused: Existing and potential investors, lenders and creditors | 🌐 Broad: Primary report users (e.g. investors, government, academics) and others affected by a company | 🌐 Broad: Multi-stakeholder audience |

| Materiality focus | 💰 Financial materiality | 💰🌎 Double materiality (impact and financial) | 🌎 Impact materiality |

| Mandatory vs. voluntary | Currently a mix. Increasingly mandatory across different jurisdictions. | Mandatory for companies in scope of the Corporate Sustainability Reporting Directive (CSRD).

+ Some out-of-scope companies are voluntarily publishing ESRS reports, signalling to the value of a double materiality approach while demonstrating transparency and leadership. |

Voluntary |

5. Should my company use the ISSB Standards?

First things first: Is ISSB reporting a legal requirement for your company, or will it be soon? As of July 2025, more than 30 jurisdictions either require some level of ISSB reporting or are considering if and how they will mandate it.

Depending on where you are, what you need to disclose will look different. For example, China is taking a double materiality (instead of just financial) approach to ISSB-aligned reporting, and Australia is adopting only the climate requirements. Meanwhile, the UK is looking at adopting the full set of ISSB Standards, with just six adjustments — including, for example, modifying the length of permitted transition periods.

If ISSB reporting isn’t legally required for your company, but you’re looking to align your sustainability reporting with what leaders are doing and / or what makes most sense for your business, consider:

- Are there any other reporting regulations (global or regional) we need to consider? As sustainability reporting regulations increasingly pop up across the globe, work with your legal / compliance team to understand which ones will affect your company and how you report.

- Who are our key audiences? The ISSB focuses on the investor audience for sustainability reporting. Consider whether you want to reach your other audiences (e.g. employees, customers, industry) through your core report or other communications.

- Where do we want to position ourselves in the sustainability landscape? The transparency and completeness of your reporting will signal the maturity and ambition of your company’s sustainability strategy. If you want to show strong commitment, voluntarily applying a globally respected framework like the ISSB could be a smart move — bearing in mind that it has less impact materiality focus than other frameworks such as ESRS and therefore may not meet all audience needs.

- What information do we currently report? Understand what sustainability information is readily available for reporting. Mapping this against the ISSB disclosures and other frameworks you are considering reporting against will help you understand how much work is needed to close the gaps.

We’d love to help

We’d love to support you to evolve your reporting, no matter what stage in the journey your company is at.

Context has supported organisations worldwide with their sustainability strategy and reporting for 25+ years — from strategic visioning and action planning, through to report conceptualisation, writing and design, and delivery. With reporting regulations on the rise, we support companies to navigate the complex landscape, understand what new reporting frameworks (for example, the ISSB and ESRS) mean for them, and assess readiness.

If you could use a hand, get in touch with Helen, Managing Director at Context Europe, at helen.fisher@contexteurope.com.