Protecting nature: The new standard for luxury fashion

Luxury fashion and the natural world are closely linked. From the purity of water required in traditional leather tanning to the healthy soil needed for premium silk and cashmere, natural resources form the foundation of luxury fashion’s quality and value. However, increasingly frequent extreme weather events and shifting global temperatures highlight the growing urgency to reduce emissions and address broader environmental impacts to protect nature’s bounty.

As the regulatory landscape shifts, companies must fundamentally evaluate their nature-related dependencies, impacts, risks and opportunities, turning environmental stewardship from a philanthropic exercise into a core pillar of risk management and overall business strategy.

Why carbon reduction targets aren’t enough

For the past decade, corporate sustainability has focused heavily on reducing greenhouse gas emissions and net zero commitments. While decarbonisation remains critical, carbon tunnel vision leaves luxury fashion companies vulnerable when it comes to natural resources. The conversation is now decisively shifting toward achieving nature-related goals that actively protect and restore biodiversity, water resources and soil health.

Regulatory and market pressures are accelerating this shift. The Taskforce on Nature-related Financial Disclosures (TNFD) is an emerging framework that has driven the adoption of nature-related disclosures globally. Since its publication in 2023, 700+ organisations have published TNFD-style reports, though many still struggle to grasp their nature-related dependencies, impacts, risks and opportunities across the full value chain. To effectively map and evaluate these complexities, we recommend that luxury fashion companies look to the official TNFD framework and guidance for a structured and guided approach. You can also refer to our article on TNFD and nature reporting.

Understanding the financial value of nature

There will be an ever-greater drive to assess the financial impact of sustainability issues. That means understanding the value of nature to the business. For example, what is the revenue impact from disruption to raw material supplies making it impossible to produce a key product line. Alternatively, what premium could be added to garments made from fully traceable cotton?

Quantifying these risks and opportunities is critical to align with the International Sustainability Standards Board (ISSB) IFRS S1 standard, as well as for companies required to report under the EU Corporate Sustainability Reporting Directive (CSRD).

If a luxury brand relies on a specific region for high-grade leather and that region faces severe water scarcity, that is not just an environmental issue — it is a direct threat to the cost of goods sold and future revenue.

Investing in nature restoration and mitigation

Changing climate conditions, economic headwinds and geopolitical events have all recently highlighted the need for resilient supply chains to support the longevity of businesses. For luxury fashion companies, strengthening supply chain resilience can take several forms:

Nature-based solutions. Supporting wetland and mangrove restoration, soil carbon projects and rewilding can stabilise raw material sourcing, sequester carbon and improve biodiversity. To align with best practice, efforts should be locally grounded and linked to key resource supply areas.

Regenerative agriculture. Investing in regenerative agriculture for key materials — such as wool, silk, cotton and leather — ensures that farming practices restore rather than deplete the local ecosystem. Benefits include improvements in soil health, carbon storage and resilience to extreme weather.

Water stewardship. As a water-intensive industry, adopting sustainable water management is critical for luxury fashion. These practices help mitigate production disruption and the physical risks posed by climate change. Consider investing in water recycling systems, drip irrigation or waterless dyeing technologies.

Circular resource use. Embedding circular design reduces raw material dependency and supply chain volatility. Think about using alternative materials in design, expanding repair programmes and investing in resale platforms to futureproof your value chain.

Communicating with authenticity

When it comes to communicating nature-related impacts and initiatives, 2025 proved that it’s not what you say, but how you say it. It has never been easier to distinguish between those companies that are genuinely committed and those that are playing lip service to sustainability.

It doesn’t need to be a data-heavy exercise that loses the core narrative. The key to credible communication is to join the dots. Strong reporting makes the connection between actions and impact. It must clearly articulate how a shift toward regenerative sourcing not only protects local waterways but also shields the business from water shortages in the long term. This transparency fosters trust. Our 2025 Luxury Fashion Sustainability Benchmark found that nature-related reporting is increasing across the industry, with companies such as Kering and LVMH aligning their actions and goals with science-based guidance on nature.

Next steps for the year ahead

To build a robust, nature-positive strategy in 2026, we recommend that luxury fashion companies focus on the following:

Increase cross-functional engagement: Political, financial, legal and environmental risks can’t be siloed. Intensify your efforts to collaborate with and engage senior colleagues, particularly those in finance, to assess nature-related risks and opportunities.

Invest in intelligence: Risk management is an ongoing process that involves monitoring environmental and social risks alongside political, economic, and regulatory developments to assess their impact. This necessitates up-to-date information on all aspects of the supply chain.

Focus on delivery: Don’t wait for perfect data. Continuing to act and engage on the issues that are material to your business will help to reduce business risk and lessen negative impacts. Nothing convinces sceptics more than tangible action.

How Context Sustainability supports nature-based reporting

Context Sustainability helps companies integrate TNFD and nature-related issues into their sustainability reporting. Our team assists with value chain mapping, materiality impact assessment, data collection and reporting aligned with frameworks, such as CSRD, GRI, SASB, and ISSB. We support clients as they develop governance systems, evaluate risks and prepare disclosures that reflect best practice. Companies preparing for upcoming reporting cycles can work with us to build a transparent, evidence-based approach to nature reporting.

Beyond the first tier: Mapping your full supply chain

For decades, luxury fashion companies have guarded their supply chains as closely as their design archives. However, recent economic and political events – including global conflicts, trade tariffs and currency fluctuations – have highlighted the urgent need for resilient supply chains.

As expectations around environmental and social performance intensify, companies are finding that guarding their supply chain from view is no longer a competitive advantage. It is a profound business risk. The challenge now lies in mapping these complex networks beyond direct business partners (sometimes known as Tier 1). But in moving from secrecy to transparency, companies need to be mindful to do it in a way that is credible, proportionate, and aligned with the organisation’s operating model.

Ending the culture of secrecy

The traditional culture of secrecy around sourcing and artisanal partnerships is increasingly at odds with stringent regulatory demands and shifting stakeholder expectations for greater supply chain visibility.

For luxury fashion brands, disclosing manufacturing partners and material origins is now a baseline requirement for maintaining market confidence, mitigating geopolitical risk, and defending corporate reputation. To get started, we recommend following some initial key steps to help map your supply chain:

Identify your direct (Tier 1) suppliers and their partners. Work closely with your procurement team and engage your suppliers to determine their locations and business relationships.

Collate and organise supplier data. Gather information on locations, labour conditions, policies and certifications. Take time to organise the data at the outset, so it can be monitored, is easy to keep up to date and provides a foundation for future reporting.

Assess key risks. Identify hotspots for sustainability issues at the country, sector, or site level and prioritise action areas. Partner with suppliers in key hotspots to amplify the impact of any initiative.

Monitor and strengthen supplier performance: Regularly review your supply chain, embedding strict due diligence processes and sustainability requirements into all supplier contracts. Work with suppliers to collect data on practices and performance, boosting product traceability.

As regulatory requirements expand, new tools are emerging to support verifiable transparency. The Digital Product Passport (DPP) is a prime example.

Under the EU’s Ecodesign for Sustainable Products Regulation, a DPP must accompany all apparel items, , documenting their environmental journey from raw material extraction to the shop floor. It functions as a digital identity card, storing data on material composition, origin, environmental footprint and the potential for an item to be repaired, reused or recycled.

For luxury fashion companies, the introduction of DPPs is not just a compliance exercise. It is an opportunity to demonstrate commitment, guarantee craftsmanship and document environmental stewardship, building trust with consumers. It also has clear business benefits. Embracing efficiency and circular resource use is increasingly important to control costs and maintain commercial advantage.

Working with suppliers on real-time data

Achieving full supply chain visibility requires a fundamental shift in how luxury fashion companies engage with their partners. The traditional model of annual, tick-box supplier audits is becoming insufficient for managing modern sustainability risks. Companies must move toward active, real-time monitoring of water usage, energy consumption and labour conditions across the entire value chain.

This transition requires investment in shared data systems and collaborative, long-term supplier relationships. When working with suppliers, keep these practical steps in mind:

Focus on the detail: Granularity is key to data that can be used for both external reporting and internal business decisions. You need precise metrics on environmental and social impacts at the facility level to support accurate disclosures.

Prioritise action over perfection: Do not wait for perfect data to begin working with your suppliers. Continuing to act and engage on the issues that are material to your business will help to reduce business risk and lessen negative impacts.

Increase cross-functional collaboration: Supply chain risk cannot be siloed within the sustainability or procurement teams. Intensify your efforts to collaborate with and engage senior colleagues, particularly those in finance, to assess the financial impact of supply chain vulnerabilities.

Mapping your full supply chain is a complex but necessary evolution. By building data systems that produce traceable, verifiable information, luxury fashion companies can establish supply chain approaches that are credible today and adaptable as expectations continue to evolve.

How Context Sustainability can help luxury fashion map the full supply chain

Context Sustainability supports companies in mapping out their entire value chain, helping inform strategy, risk management and double materiality assessment. Our team can assist with clear stakeholder engagement plans with direct and indirect suppliers to ensure that you are continuously monitoring and improving supplier performance. We help our clients with target setting to address the most pressing supply chain issues that link with existing frameworks and standards.

New rules for luxury: A simple guide to CSRD for fashion brands

The reputation of the world’s luxury fashion companies has been built on heritage, craftsmanship and exclusivity. Today, that reputation is being increasingly shaped by the degree of transparency about sustainability practices in their operations and supply chains. Stricter regulatory frameworks, such as the EU’s Corporate Sustainability Reporting Directive (CSRD) are shifting sustainability from a ‘nice-to-have’ to a central driver of corporate decision-making and governance. Responding effectively requires an understanding of both regulatory direction and the wider business context for sustainability.

From voluntary to mandatory reporting

CSRD raises the sustainability reporting stakes, swelling the number of topics that must be covered. It’s no longer enough to highlight positive initiatives — such as supporting local artisans or launching limited collections that centre on using more sustainable materials — while keeping more complex supply chain challenges out of the public eye. Under CSRD, sustainability disclosures are given the same weight as financial reporting.

The first flurry of CSRD-aligned reports arrived at the start of 2025. This included reports from leading fashion companies, such as Kering, LVMH and Brunello Cucinelli. Some of these were lengthy, compliance-heavy documents where the uniqueness of each company’s sustainability transformation got lost. For more insight on how luxury fashion companies addressed these and other issues in their reporting, read our latest Luxury Fashion Sustainability Benchmark.

While the EU Omnibus simplification package will lead to disclosures being stripped back, key lessons from the first two years of reporting still apply:

Narrative matters. While disclosures must meet legal thresholds, companies still need to communicate their vision and strategy in a clear and compelling way. It is critical to engage other stakeholders, such as customers and employees, as well as show investors how companies are innovating and building long-term resilience.

Collaboration and preparation are key. The scope of CSRD is broad and putting together comprehensive disclosures takes cross-functional collaboration. That means starting early to get the right people involved. We offer tips on engaging others in the reporting process in Sustainability reporting: All hands on deck.

Materiality shapes everything. Materiality is the foundation of CSRD. Luxury fashion companies must have a clear view of what matters to their stakeholders.

Understanding double materiality

The concept of double materiality is at the heart of CSRD. For luxury fashion companies, this means looking at sustainability topics from two perspectives – their environmental and social impact and how sustainability risks and opportunities affect the financial bottom line.

A robust materiality assessment is crucial for understanding the sustainability issues that actually matter to a business. Companies in the luxury fashion sector should consider :

Impacts. Assessing impact materiality (sometimes referred to as the inside-out perspective) is about understanding how the company’s activities affect the world. This includes the environmental footprint of sourcing raw materials (such as leather, precious metals or cashmere), the carbon intensity of manufacturing and the labour conditions in global supply chains.

Financial risks and opportunities. Financial materiality (also known as the outside-in perspective) explores how sustainability issues impact company financial performance. This includes the financial risks of climate change disrupting agricultural supply chains (e.g. silk or cotton shortages), or impending carbon taxes eroding profit margins. It’s also about how responding to evolving consumer sentiment can open up new revenue opportunities, e.g. from embracing rental models.

Because all major reporting frameworks have materiality at their core, keeping your materiality assessment up to date is a critical tool to help you stay on track as regulation evolves. We provide our top tips in 7 steps to conduct an effective double materiality assessment.

Getting your sustainability data audit-ready

Under the CSRD, sustainability reporting is subject to limited third-party assurance, or audit, ensuring claims are verifiable and data accurate. Given the scope of reporting, it’s no longer possible to rely on isolated metrics or fragmented spreadsheets. Sustainability data must meet the rigorous standards traditionally reserved for financial accounting.

We recommend the following steps to ensure your data is audit-ready:

Granular data collection. Credibility comes from hard data. Review your sustainability metrics to verify you are collecting detailed information against each of your targets. Granularity is key to having data that serves both external reporting and internal business cases.

Cross-functional engagement: Environmental and social risks cannot be siloed. Closer collaboration between sustainability, finance and legal teams is essential to evaluate different outcomes and embed accurate data collection into daily operations.

Document the process: Don’t forget to thoroughly document your data collection methodologies and processes. Providing clear evidence trails is non-negotiable as more countries require assurance of sustainability reports.

The current regulatory landscape may feel like a tug-of-war, but the business case for robust sustainability practices remains clear. By treating the CSRD not just as a compliance exercise, but as a framework to strengthen governance and risk management, luxury fashion companies can build resilience and maintain their prestige in a highly scrutinised market.

How Context Sustainability can help luxury fashion transition to CSRD

Context Sustainability supports companies on their journey towards full CSRD-alignment. Our team helps companies to complete in-depth ESRS gap analysis, double materiality assessments that analyse value chain impacts, risks and opportunities, plan clear stakeholder engagement and end-to-end CSRD reporting and management. We help clients link their CSRD approach with existing frameworks, including GRI, SASB and IFRS S1 and S2.

5 common issues with carbon removal credits and how to avoid them

Carbon removal credits can be a useful tool for companies to meet their net-zero targets. They also help scale solutions needed to address wider climate and nature challenges. And large-scale removal of carbon dioxide from the atmosphere is required to limit global warming to 1.5˚C. But the voluntary carbon market (VCM) used to buy and sell carbon credits faces several key challenges, including concerns around quality, supply, and greenwashing.

For companies investing in climate solutions, this may leave them between a rock and a hard place. Here we provide an overview of the common pitfalls and some practical advice on how to avoid them.

Feeling confused? See the jargon buster below for an explanation of key terms.

How should carbon removal credits be used?

Carbon dioxide removal (CDR) is not an alternative to deep emissions reduction, but it can be used in parallel to complement mitigation activities. Under the Science Based Targets initiative (SBTi) guidance, companies must reduce greenhouse gas (GHG) emissions across their full value chain by at least 90% from their baseline year to achieve net zero. Carbon removal credits can be purchased to remove and store the remaining 10% of unavoidable emissions.

Are companies still investing in carbon removals?

The VCM’s heyday is waning, but carbon removals are not. MSCI found corporations used credits worth a total of $1.4 billion in 2024, compared to $1.7 billion in 2022. But companies have increasingly been choosing higher-quality carbon removal credits over cheaper carbon avoidance credits, and MSCI projects the removal market will rise to $4–11 billion by 2030.

What’s being done to restore faith in the market?

The VCM is key to enabling large-scale private funding of carbon removal projects. It complements public finance, which is not enough to reach global net-zero targets by itself. To stimulate investment, several governments are promoting high-quality carbon credits. In April 2025, the UK launched a consultation on its carbon credit integrity framework, and in June, Singapore issued draft guidance on using carbon credits voluntarily.

Beyond government initiatives, the SBTi recently released its draft Corporate Net-Zero Standard V2, which encourages early uptake of carbon removal credits. The guidance includes a ‘removals target’ for scope 1 emissions, whereby companies gradually increase their use of carbon removals over time until all residual scope 1 emissions are matched by the net-zero target year.

Practical steps to overcome common challenges

1. Addressing quality and additionality concerns

There are several factors that can affect credit quality, such as lack of governance, tracking, short removal timescales, and additionality (i.e. projects would not have occurred without the carbon credit). Several companies have been criticised for purchasing “worthless” carbon credits that do not deliver real climate benefits, for example funding projects that would have occurred anyway.

Ensuring project due diligence, tracking, verification, and certification is crucial when choosing which credits to buy. There are a range of legitimate guidelines available to help you, including:

Integrity Council for the Voluntary Carbon Market (ICVCM).

The ICVCM has developed 10 principles to help identify carbon credits that create verifiable climate impact, such as third-party validation, permanence, and robust quantification.

Beyond confirming the integrity of each credit, you should consider your credits as a portfolio. Projects originally considered high quality could fail to live up to the initial expectations. Like other investments, diversifying your portfolio reduces overall risk.

2. Navigating the lack of standardisation

A wide range of projects and credit providers are available, with varying levels of quality. The lack of standardisation can lead to confusion, undermining market confidence and making it challenging for companies to gauge the impact and credibility of a project.

Look out for leading carbon credit providers that conduct their own due diligence on each project and ensure they’re verified by internationally recognised carbon certification standards. Some of the most widely recognised certification standards include Gold Standard and Verra’s Verified Carbon Standard (VCS).

3. Securing a shrinking supply

Demand for high-quality carbon removal projects is on the rise but supply is limited. Purchasing credits close to your net-zero target date could risk sky-high prices as many companies race to secure the dwindling reserves.

To secure carbon credits before the price is too steep, you can use carbon forward contracts, purchasing credits now to remove GHG emissions in future years. This provides a fixed price and helps fund projects that need financing to scale. But it’s worth considering the uncertain future impact of these investments as climate science is rapidly evolving.

4. Overcoming budget constraints

Companies should prioritise investing in GHG emissions reductions over credits. But most companies, particularly those in hard-to-abate sectors, will need carbon removal credits in future to balance out the remaining 10% of their emissions. For some, budget could be an issue, even without the risk of prices for high-quality credits skyrocketing the nearer we get to 2050 (assuming there are any left).

Besides carbon forward contracts, there are high-quality projects with a lower price tag. These projects often involve nature-based carbon removal methods, such as reforestation. But make sure to avoid purchasing cheap, low-quality carbon credits by ensuring project due diligence and certification, as these may not have the impact they claim and risk greenwashing allegations.

5. Avoiding reputational risks

Fossil fuel companies dominated the VCM in 2024,[1] raising concerns that companies are misusing carbon credits without reducing their own GHG emissions. Companies have faced heavy backlash for using low-quality carbon credits to make GHG emissions reductions or carbon-neutral claims.[2]

To avoid greenwashing risks, steer clear of using credits to make GHG emissions reduction, net-zero, or carbon-neutral claims. Instead, transparently report on credits used and distinguish these disclosures from your GHG emissions reporting. Include specifics on the volume and type of credits purchased, project location, purpose of use, third-party certification, and technical details.

See the European Sustainability Reporting Standards (ESRS), International Financial Reporting Standards (IFRS), and Global Reporting Initiative (GRI), for guidance on how to report on carbon removals (ESRS E1-7, IFRS S2 36e, and GRI 102-10).

Beyond their core purpose and key challenges, carbon removal projects can provide benefits like creating job opportunities in local communities, reducing air pollution, and protecting biodiversity. Look for projects that deliver positive sustainable development impacts while ensuring best practice social and environmental safeguards are in place.

There are several ways to go about purchasing carbon removal credits, and your company’s approach depends on several factors, including the maturity of your net-zero roadmap, GHG emissions reduction progress, targets, carbon credit awareness, and budget. Context supports companies to develop and implement carbon credit and wider sustainability strategies. If you’d like to talk about your organisation’s needs, please reach out to helen.fisher@contexteurope.com.

Jargon buster

Carbon credits are a market-based tool to generate funding to remove or avoid GHG emissions. One credit represents 1 metric tonne of carbon dioxide equivalent (CO2e).

Carbon removal credits remove carbon from the atmosphere for the short, medium, or long term. These include natural carbon removals, such as reforestation projects, and technological carbon removals, such as Direct Air Capture (using technology to capture carbon from the air). Companies can use these credits to remove the remaining 10% of their GHG emissions (in addition to reducing 90% of their emissions under SBTi guidance).

Carbon avoidance credits prevent additional future GHG emissions being released into the atmosphere. They should not be used to reach net zero under SBTi guidance, but investments can be made in parallel to reduction and removal activities. Examples include renewable energy and forest protection projects.

Carbon dioxide removal (CDR) refers to human activities to deliberately remove and durably store carbon dioxide from the atmosphere. CDR includes a range of technologies, practices, and approaches, such as Bioenergy with Carbon Capture and Storage (growing and burning biomass to create energy and capture the resulting GHG emissions), that all differ in integrity, maturity, timescale, mitigation potential, cost, co-benefits and side effects.

The voluntary carbon market (VCM) operates in parallel with the mandatory carbon market, enabling companies to purchase carbon credits on a voluntary basis.

The sustainability universe is watching as the EU’s new mandatory sustainability reporting standards go through the wringer. Meanwhile, the International Sustainability Standards Board (ISSB) Standards are gaining momentum.

The ISSB, born at the 2021 UN climate conference, COP26, is responsible for building a framework for companies everywhere to report sustainability information in a consistent way. Already, 17 jurisdictions across the globe — including Australia, Brazil, Hong Kong, Mexico and Nigeria — have confirmed full or partial adoption of the ISSB’s standards. An additional 16 — including Canada, China, Japan, Singapore, Uganda and the UK — are in the process of formally adopting the framework to some degree. This group of 33 committed countries includes11 of the world’s 20 largest economies.

With the ISSB Standards picking up steam, you may be wondering what you need to know (perhaps while internally panicking at the thought of yet another sustainability reporting framework). To help get you started, here are five ISSB FAQs answered.

1. What is the purpose of the ISSB Standards?

Companies globally are increasingly expected and mandated to share sustainability information. Why? To give people who want to know about a company (e.g. customers, investors, employees, partners, rating and ranking organisations, etc.) a complete picture of its performance, progress, prospects and plans.

But there is currently no one framework telling companies which sustainability information to report. Rather, there are many frameworks asking for different types of qualitative and quantitative information. This means we’re often reading cherry-picked success stories and comparing apples with oranges when evaluating sustainability performance across companies.

The ISSB Standards aim to change this. They were developed in response to strong market demand for a global sustainability reporting baseline to give companies clear guidance on what to report. In the way that traditional financial reporting is consistent and comparable across the world thanks to common standards, the ISSB wants sustainability reporting to be the same.

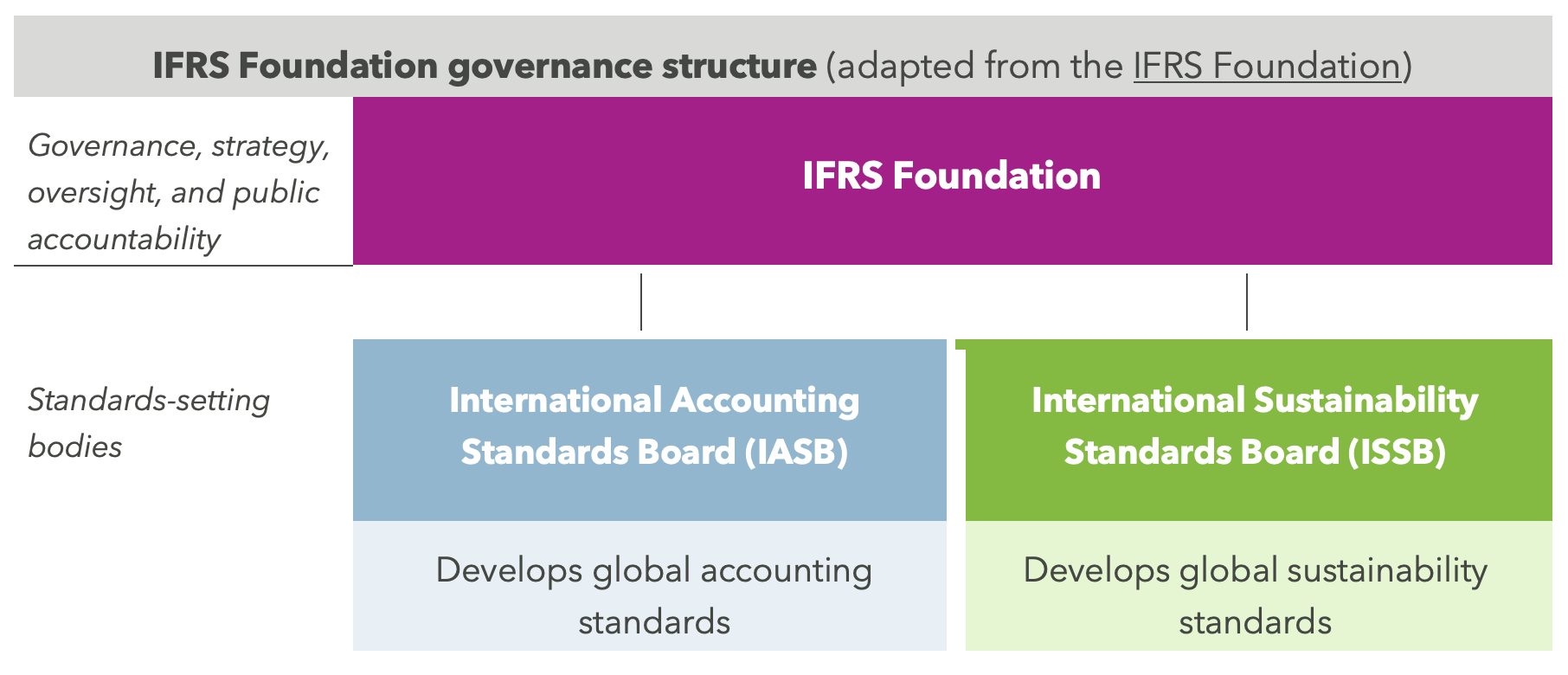

2. Who develops and oversees the ISSB Standards?

The International Financial Reporting Standards (IFRS) Foundation establishes the common global framework forfinancial reporting through the International Accounting Standards Board (IASB), its standards-setting body. In 2021, the IFRS Foundation introduced the ISSB — a new branch in charge of developing an equivalent international framework forsustainability reporting.

In the interest of developing a single global standard, several big sustainability frameworks and organisations were essentially absorbed into the IFRS Foundation — including the Climate Disclosure Standards Board (CDSB), the Task Force for Climate-related Financial Disclosures (TCFD), the Value Reporting Foundation’s Integrated Reporting Framework, the Sustainability Accounting Standards Board (SASB) Standards, and the World Economic Forum (WEF)’s Stakeholder Capitalism Metrics.

3. What types of information do companies need to report under the ISSB Standards?

The ISSB Standards are designed to provide useful sustainability information to external stakeholders who make financial decisions about a company (investors, lenders and creditors). So, they focus disclosures on sustainability-related risks and opportunities that could impact the decisions these stakeholders make. In other words, they focus on financial materiality.

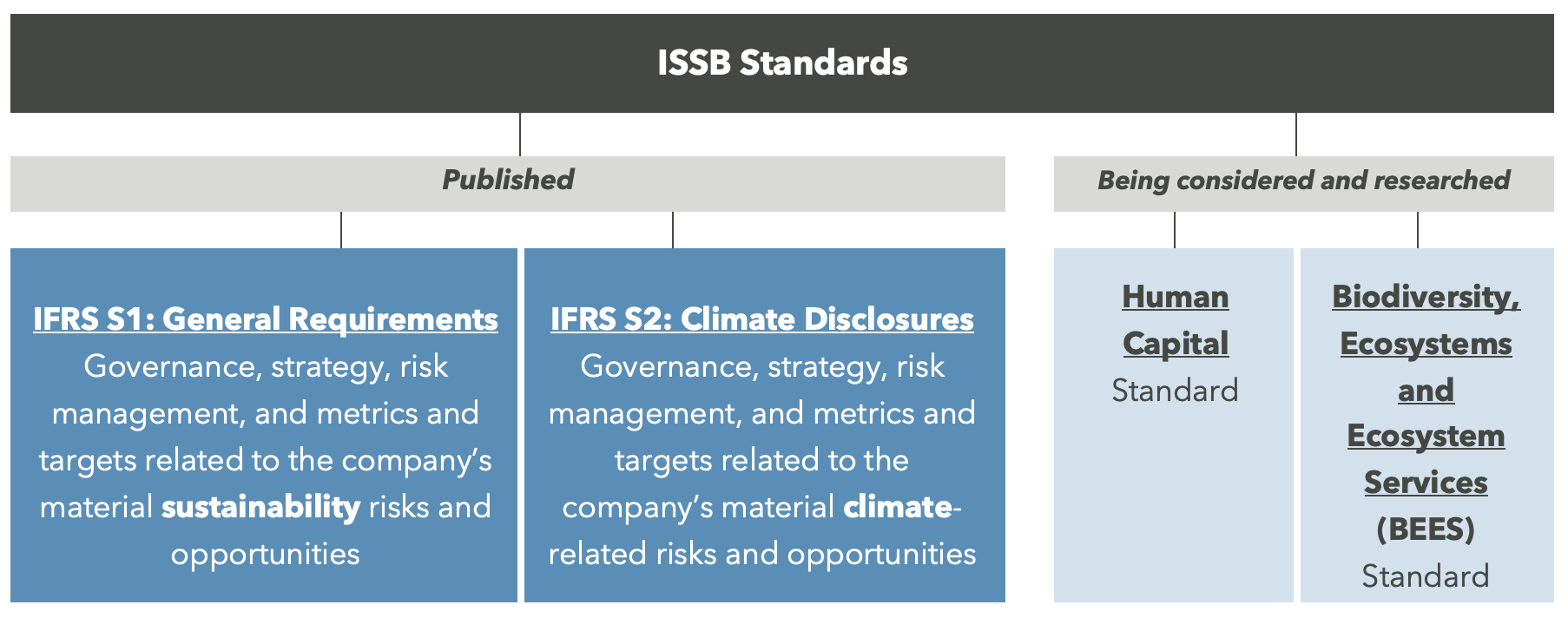

There are two active ISSB Standards — including general disclosures (IFRS S1) and specific climate disclosures (IFRS S2) — with others being explored. Both active standards ask for information on governance, strategy, risk management, and metrics and targets for financially material sustainability topics. This mirrors the structure of the TCFD recommendations, today’s most widely adopted recommendations for climate-related risk and opportunity disclosures — since absorbed into the IFRS Foundation.

4. What is the difference between the ISSB Standards and other common reporting frameworks?

While the ISSB Standards aim to be the global baseline for sustainability reporting, they currently exist in a busy space. The European Sustainability Reporting Standards and the Global Reporting Initiative Standards are the two other big players. The fundamentals that set them apart are their breadth of focus and approach to materiality, though there is a level of interoperability across all three.

International Sustainability Standards Board (ISSB) Standards

European Sustainability Reporting Standards (ESRS)

Global Reporting Initiative (GRI) Standards

First launched

2023

2023

2000

Standard developers

International Sustainability Standards Board (ISSB)

European Financial Reporting Advisory Group (EFRAG)

Global Sustainability Standards Board (GSSB)

Geographic focus

Global

EU

Global

Key audience(s)

🎯 Focused: Existing and potential investors, lenders and creditors

🌐 Broad: Primary report users (e.g. investors, government, academics) and others affected by a company

🌐 Broad: Multi-stakeholder audience

Materiality focus

💰 Financial materiality

💰🌎 Double materiality (impact and financial)

🌎 Impact materiality

Mandatory vs. voluntary

Currently a mix. Increasingly mandatory across different jurisdictions.

Mandatory for companies in scope of the Corporate Sustainability Reporting Directive (CSRD).

+ Some out-of-scope companies are voluntarily publishing ESRS reports, signalling to the value of a double materiality approach while demonstrating transparency and leadership.

Voluntary

5. Should my company use the ISSB Standards?

First things first: Is ISSB reporting a legal requirement for your company, or will it be soon? As of July 2025, more than 30 jurisdictions either require some level of ISSB reporting or are considering if and how they will mandate it.

Depending on where you are, what you need to disclose will look different. For example, China is taking a double materiality (instead of just financial) approach to ISSB-aligned reporting, and Australia is adopting only the climate requirements. Meanwhile, the UK is looking at adopting the full set of ISSB Standards, with just six adjustments — including, for example, modifying the length of permitted transition periods.

If ISSB reporting isn’tlegally required for your company, but you’re looking to align your sustainability reporting with what leaders are doing and / or what makes most sense for your business, consider:

Are there any other reporting regulations (global or regional) we need to consider? As sustainability reporting regulations increasingly pop up across the globe, work with your legal / compliance team to understand which ones will affect your company and how you report.

Who are our key audiences? The ISSB focuses on the investor audience for sustainability reporting. Consider whether you want to reach your other audiences (e.g. employees, customers, industry) through your core report or other communications.

Where do we want to position ourselves in the sustainability landscape? The transparency and completeness of your reporting will signal the maturity and ambition of your company’s sustainability strategy. If you want to show strong commitment, voluntarily applying a globally respected framework like the ISSB could be a smart move — bearing in mind that it has less impact materiality focus than other frameworks such as ESRS and therefore may not meet all audience needs.

What information do we currently report? Understand what sustainability information is readily available for reporting. Mapping this against the ISSB disclosures and other frameworks you are considering reporting against will help you understand how much work is needed to close the gaps.

We’d love to help

We’d love to support you to evolve your reporting, no matter what stage in the journey your company is at.

Context has supported organisations worldwide with their sustainability strategy and reporting for 25+ years — from strategic visioning and action planning, through to report conceptualisation, writing and design, and delivery. With reporting regulations on the rise, we support companies to navigate the complex landscape, understand what new reporting frameworks (for example, the ISSB and ESRS) mean for them, and assess readiness.

If you could use a hand, get in touch with Helen, Managing Director at Context Europe, at helen.fisher@contexteurope.com.

How the EU’s last-minute delay to its sustainability directive affects U.S. companies

What’s going on with CSRD?

In early 2025, the EU Parliament hit the brakes on the Corporate Sustainability Reporting Directive (CSRD). After years of build-up, they’ve hit pause. Why? Because of growing anxiety in Brussels over whether Europe can stay competitive under the weight of all its new regulations.

The turning point came with a 2024 Competitiveness Report, led by former Italian PM Mario Draghi. That triggered a new “Competitiveness Compass” from the EU Commission, aimed at revitalizing economic growth. As part of that compass, CSRD and the Corporate Sustainability Due Diligence Directive (CSDDD) were flagged as too burdensome.

Leaders in France and Germany piled on. French officials called CSRD “hell for companies,” while Germany’s finance minister warned it would force around 13,000 companies to track 1,000+ data points each—an especially heavy lift for small and mid-sized businesses.

In response, the EU introduced the strangely named Omnibus Proposal in February 2025 that promises two big changes:

Fewer companies will fall under CSRD

The disclosure requirements will be streamlined

To provide time to make these they’ve delayed the CSRD effective dates by two years for many companies, including U.S. firms with significant EU operations.

What this means for U.S. companies

If your company has a large EU subsidiary, CSRD originally required the subsidiary to report in 2026 for fiscal year 2025. That’s now been pushed back to 2028 (the 2029 deadline for full Group reporting remains unchanged).

To avoid juggling two different systems, many U.S. companies had decided to report at the Group level in 2026. That means a lot of teams have already spent big on:

Double materiality assessments

New data collection systems

Staff training

So now what? Do you keep pouring money into something that might change again?

Our take: hit pause (but don’t hit delete)

Let’s be real: It’s unlikely that CSRD disappears entirely, but major revisions are very much on the table. That makes further investment risky. U.S. lobbying groups are also pushing back, and trade talks between the U.S. and EU could lead to a ‘lighter’ CSRD version for American companies. Uncertainty is the name of the game right now.

A smart game plan for 2025–2029

Here’s what we recommend:

Pause further CSRD development

Don’t invest more until the EU clarifies what the new version looks like

Keep using what you’ve built

If you’ve got materiality assessments or data systems in place, use them. But hold off on new rollouts or enhancements

Stick to your existing reporting framework

Go back to the standards your company was using before CSRD such as GRI or IFRS

Stay tuned and stay nimble

We expect more updates (and hopefully clarity) from the EU later this year

Here’s a suggested calendar for US CSOs navigating the CSRD delay, designed to balance prudence with preparedness through 2029.

CSRD Delay: Game Plan for 2025–2029

Need help with your sustainability reporting?

Context has been at the forefront of sustainability reporting since 1997, with over 500 reports completed. Based in the US and UK we are always up-to-date with the latest regulations, standards, and innovations in the field.

If you would like to talk about the best path through the CSRD uncertainty for your company, we’re here to help. Please send me an email (simon@contextamerica.com).