For more than three decades, sustainability enjoyed a steady rise. From the 1990s onwards, the direction of travel was clear: forward and upward. Influential companies embraced sustainability, creating dedicated departments and appointing Chief Sustainability Officers—a role that barely existed a decade ago and is now both recognized and well-compensated.

This shift brought real change. Companies began measuring their impacts, disclosing performance, and setting improvement goals. In many ways, sustainability became a modern industrial revolution.

But just as it seemed sustainability had reached critical mass, the momentum stalled. Today, for the first time, we are facing a concerted pushback. What is our survival strategy?

What’s Changed?

Two powerful forces have converged:

The rise of populist politics in the U.S. and across Europe.

The retreat from globalism in favor of economic nationalism.

These shifts are reshaping the business and regulatory environment for sustainability—and not in our favor.

America and Europe: A Regulatory Reversal

In the United States, environmental and social protections have been rolled back, regulatory agencies weakened, and outspoken opponents of climate action, ESG, and DEI placed in positions of power.

The EU “U Turn” on Green Deal Regulations CSDDD and CSRD

Europe is now following suit. Germany and France, longtime champions of ambitious green policy—are calling for a pause or rollback of key components of the EU Green Deal. Following a competitiveness review led by former Italian Prime Minister Mario Draghi, pivotal regulations like the Corporate Sustainability Reporting Directive (CSRD) and the Corporate Sustainability Due Diligence Directive (CSDDD) are being stalled. Others may soon follow in what some describe as a “bonfire of EU sustainability regulations.”

ESG Investment Is Losing Steam

Meanwhile, another major driver of corporate sustainability is also in decline: ESG investing. Since 2024, ESG fund flows have reversed, sending a clear and troubling signal to corporate boardrooms—especially in an environment where every dollar must be justified.

These headwinds have led sustainability pioneer John Elkington to dub the current moment a “sustainability recession.”

Why Traditional Best Practices Need Updating

We are entering a new era where “business as usual” in sustainability no longer works. Many in the field seem caught off guard, clinging to the belief that a change in political leadership in a few years will reset the trajectory. That’s wishful thinking.

Sustainability professionals must face reality:

Have current strategies truly achieved their goals?

Are sustainability budgets being deployed as effectively as possible?

Can we always justify our programs with a robust business case?

The honest answer: “Could do better.”

A Strategy for Survival

We can’t ignore the democratic outcomes in multiple Western nations. We may not share the views of populist governments, but rejecting or resisting them outright is counterproductive. Instead, we must engage—with pragmatism.

This means reframing sustainability in business terms—efficiency, innovation, competitiveness, risk reduction. It also means listening to public concerns, especially when sustainability is viewed as elitist, remote, or economically burdensome.

Strengthening the Business Case: Ten Steps to Recalibrate Your Sustainability Strategy for Your C-suite

For years, corporate sustainability operated on the assumption that it would inevitably become a business imperative. Companies often approved budgets without hard ROI calculations—believing it was smart to get ahead of the curve.

But today, that certainty is gone.

In an era of budget pressure, tariffs, and shifting political winds, sustainability teams must work harder to prove value. The challenge now is clear: build a stronger business case—or risk losing relevance.

Below are ten practical ways to future-proof your sustainability strategy and reporting, bringing it in line with today’s corporate decision-making.

1. Simplify Processes

Sustainability is known for its complexity. Standards like GRI, SBTi, and ESG ratings are valuable, but not always efficient.

In a leaner operating environment, it’s time to be more strategic. Focus on the standards that matter most to your stakeholders—and streamline the rest. Less process, more impact.

2. Leverage Financial Metrics

Too many sustainability programs still measure environmental and social efforts without the associated financial impact.

Now is the time to track financial benefits—like energy savings, waste reduction, and material efficiency. Quantifying cost savings helps make the business case in language that resonates with the C-suite.

3. Show the Brand Benefit

Sustainability often strengthens brand trust—but this impact is rarely measured.

Work with marketing and insights teams to quantify how your efforts shape reputation. Use data from consumer research, sentiment tracking, and brand equity studies to connect the dots.

4. Integrate with Risk Management

From supply chain disruption to regulatory risk, sustainability plays a clear role in managing uncertainty.

Make that role visible. Embed it in your company’s risk disclosures and financial reports. Investors increasingly expect to see how sustainability enhances resilience.

5. Re-position Sustainability as a Competitiveness Strategy

Sustainability isn’t just about mitigating risks—it can spark innovation and open new markets. Customer preferences, especially among younger demographics and B2B buyers, are shifting toward sustainable products and services.

Highlight where your efforts are driving product innovation, differentiating your brand, or creating new revenue streams.

6. Strengthen Supply Chain Resilience

Sustainable sourcing, circular design, and supplier engagement can fortify supply chains against shocks—such as price volatility, geopolitical instability, or resource scarcity.

In a world of disrupted logistics and rising raw material costs, sustainability can demonstrate a competitive advantage in procurement and continuity planning.

7. Put a Value on People Investment

Employee-focused programs—like training, wellness, and inclusion—are often justified with soft metrics.

That’s no longer enough. Start measuring ROI by linking these programs to retention, productivity, and innovation outcomes. Data helps justify continued investment.

8. Reconnect sustainability with Economic Fairness

Many populist movements are fueled by economic disenfranchisement. Sustainability must show how it benefits workers, communities, and consumers—not just investors or the environment.

Frame sustainability as a force for local job creation, energy independence, cost-of-living relief, and community investment.

9. Focus on National Interest and Security

In a nationalist era, linking sustainability to national resilience is a powerful frame.

Emphasize reducing reliance on imported fossil fuels, reshoring clean-tech supply chains, and mitigating climate risks that affect food security or disaster preparedness.

10. Streamline Your Reporting

Sustainability reporting has become a resource-heavy exercise, often diverting attention from real-world change.

Rethink your reporting approach. Focus on what’s required, relevant, and meaningful. Then automate and consolidate wherever possible. The goal: more substance, less time.

Conclusion: Adapt to Stay Relevant

Corporate sustainability isn’t dead—it’s evolving. In today’s environment, sustainability must pull its full weight in business terms—contributing to growth, efficiency, innovation, and risk management. This is not about abandoning principles. It’s about reframing sustainability as a driver of value—and making sure that value is visible, measurable, and aligned with the times.

Need help recalibrating your sustainability strategy and reporting?

Get in touch to explore how your team can build a more resilient, results-driven program for 2025 and beyond. simon@contextamerica.com

If it takes a village to raise a child, then it takes a cross-functional team of enthusiastic experts to create a comprehensive sustainability report. But for many outside the core reporting team, the process can seem dry and a distraction (or unwanted diversion) from the day job.

As reporting requirements continue to evolve globally, it has never been more important to engage a wider group of colleagues. Sustainability professionals are under pressure. Around 70% suggest that the growing reporting burden is taking them away from delivering on-the-ground action and making progress towards company targets — a trend that will only intensify as the scope of mandatory requirements broadens.

Many sustainability specialists also suggest they are not best placed to lead on reporting. They are change agents, not risk managers.

Knowing the difference between standards

If this sounds familiar, how do you escape being stuck in ‘reporting mode’ for eternity?

Part of the answer lies in knowing the regulations — understanding the common denominators between requirements and the subtle differences. The Corporate Sustainability Reporting Directive (CSRD) and the IFRS Sustainability Standards claim to be interoperable. But the former mandates a double materiality assessment — the latter a single materiality approach assessing an issue’s impact on company financial performance. A CSRD-aligned double materiality assessment is likely to meet IFRS requirements, but not the other way around.

It’s essential to think about different reporting requirements. One framework might require you to report on renewable energy as a share of total usage and another on the source of your renewable energy. Understanding these differences makes it possible to collect the data once to comply with both rules.

Even with the best planning, knowing exactly the information you need, you have to source it from somewhere. And that means engaging the wider business — no mean feat when many teams regard sustainability data collection as dull and a distraction. So how do you break the log-jam?

Getting engaged

Resistance is normal and often stems from a lack of knowledge. Why should employees get involved? What’s in it for them? How will it help them day to day to do their job better? Here, communication, training and support are essential. And explaining issues in terms that resonate for them rather than talking explicitly about ‘sustainability’ helps.

Employees want to help build a more sustainable business — you need to explain how reporting fits into that. It’s about giving them an understanding of the regulations and the growing trend towards mandatory reporting. They need a sense of what data is required now, as well as visibility into you will be looking for in future as rules tighten, so they can have an input into the best way to collect the data.

If you work for a privately-owned company, it’s worth highlighting the temporary crunch point that comes from having to face mandatory reporting for the first time. This forces your business to play catch-up with listed companies which have been reporting for many years.

Making sustainability relevant

But, above all, you need to sell the benefits to them and how it will help them to do their job better. That means tailoring the benefits to each role.

Sustainability helps to build resilience, improve efficiency and reduce costs — music to the finance team’s ears. It also drives revenue and attracts talent — great for HR. But only if customers and potential employees are aware of your efforts and convinced of your progress. Without data, the company’s sustainability story can quickly descend into greenwashing.

Procurement teams face increasing requests from customers, suppliers and business partners for sustainability data. Their support in collating data makes that process easier. They also gain the skills and knowledge they need to support suppliers to comply with your data requests, strengthening those business partnerships.

Celebrating progress

You can’t manage what you can’t measure. Your sustainability data is part of that picture, allowing you to track progress and prioritise action. It’s important to show employees how it will help them focus on what matters and do their job better — not just how it benefits the business. It could be used to direct their efforts to decommissioning old equipment and saving energy, rather than spend time on a business case for new equipment when there’s limited budget to invest. This would spare them the frustration of having their proposal knocked back after hours of work.

Most importantly, reporting is about celebrating success. It demonstrates company — and team — progress. Supporting with data collection is their chance to showcase the good things that are going on within their team and function to the rest of the business and the wider world.

Employee engagement is tough and takes time. But, faced with The added understanding of your sustainability strategy which comes with engagement also helps drive action, shift your business towards being more sustainable, and realise your targets.

Context supports companies to tell their sustainability story — working in partnership to help identify and demonstrate progress from across the business. If you would like to talk about your organisation’s needs, please get in touch via www.contextsustainability.com or helen.fisher@contexteurope.com.

2024 has been marked by growing regulation — increasing sustainability reporting requirements and legislating issues from nature to supply chain due diligence. And with most businesses experimenting with artificial intelligence (AI), regulators also attempted to rules in place.

While the focus for years has been on climate and the environment, social issues gained greater attention. Two-thirds of companies expect to spend more on addressing social sustainability over the next few years.

As we embark on a new year, Context reflects on the events of the previous 12 months and what they mean for business. We also consider what lies ahead and how best to prepare.

01. Growing commitment to protect and promote nature

New frameworks and benchmarks increase the structure on assessing nature impacts, but concrete actions are still lagging.

Despite the pledges, there’s still some way to go. Of the companies reviewed in Nature 100’s first benchmark, two-thirds have a nature commitment — for 45%, this covers the full value chain. But only 13 organisations have kicked off a comprehensive materiality assessment.

In 2024, European regulators reinforced the need for greater action, approving the EU Nature Restoration Law. Member States must create National Restoration Plans aiming to restore at least 20% of degraded areas by 2030. The EU later delayed the Deforestation Regulation by 12 months as smaller suppliers struggled to implement the necessary due diligence.

Top tips to prepare for the year ahead

Conduct a materiality assessment. Understand your nature-related impacts, risks and opportunities, so you address them.

Develop a holistic, integrated strategy. Taking a comprehensive approach to nature strategy embeds it into the wider sustainability strategy and business model.

Set targets to restore and prevent biodiversity loss. Aligning with SBTN guidance will ensure targets are relevant, measurable and support international ambitions to reverse biodiversity loss by 2030.

02. Circularity comes of age?

The 2024 Circularity Gap Report officially declared the circular economy a megatrend.

More than one-third of Fortune 100 companies are expected to announce circularity goals within the next 12 months. Pressure is mounting on more companies to follow suit — especially the 40,000 private companies and smaller businesses coming within scope of the Corporate Sustainability Reporting Directive from 2026. They need to assess the importance of resource use and circular economy for their business as part of a full double materiality assessment.

National governments are also aiming to stimulate circular thinking across the economy. To date, more than 75 countries have a national circular economy action plan in place — another 14 are in the pipeline. While broadly welcomed, there are growing concerns about potential loopholes — for example, due to differing rules on export of electronic waste.

Explore how circularity supports wider strategy. Reduced resource use has significant cost benefits as well as helping to deliver wider sustainability ambitions. Define your circular ambition and set quantifiable targets.

Educate employees on circularity. Ensure design teams have the knowledge and skills they need to design products and services to use fewer materials and with repair, reuse and recycling in mind.

Seek out cross-industry collaboration. The transition to a circular economy will require systemic change, only achievable through widespread partnership and collaboration.

03. AI dominated the headlines

Artificial intelligence (AI) has been widely adopted, but regulation is only just starting to catch up.

As 2024 progressed, the environmental impacts of this rapid technology growth became clear, with the UN Environmental Programme publishing the most detailed lifecycle assessment to date. It revealed, for example, that AI could represent 35% of Ireland’s energy use within the next year.

As use of AI has grown so too has concern about its ethical, social and environmental impacts. The EU approved the Artificial Intelligence Act, requiring human monitoring of all systems. Stricter standards apply to high-risk applications for health, education, work and critical infrastructure. The Act also calls for standards and reporting on energy efficiency to reduce AI’s environmental impact.

Colorado became the first US state to legislate on AI, while Senator Markey introduced the federal Artificial Intelligence Environmental Impacts Act 2024 to accelerate study of AI impacts and stimulate voluntary reporting.

This regulatory push will mean that businesses and governments will have to get to grips with the issues around AI in 2025 and put plans in place to address negative consequences. To build and maintain customer trust, AI will need to be deployed ethically, securely and transparently, while minimising bias.

It’s also time to focus on the business benefits. Stakeholders want to hear how organisations are using AI to deliver positive results — whether to augment products, optimise processes or create better offerings for customers.

Top tips to prepare for the year ahead

Familiarise yourself with emerging standards. Initiatives including the Software Carbon Intensity standard aim to bring a harmonised approach to measuring AI impacts.

Ensure robust governance. The EU AI Act will come into full force in early 2026. Now’s the time to ensure policies and processes are in place guiding responsible AI use.

Start collecting data. While reporting is currently voluntary, there are growing moves to track AI’s energy use. 2025 is the year to start measuring.

04. Social issues are still overlooked by many companies

Companies and regulators are increasingly shining a spotlight on social issues.

Companies spend one-third of their time and sustainability budget on social issues — and around 40% on environmental challenges. Despite 66% of companies in the US and Europe predicting growing budgets for addressing social sustainability challenges, 26% have little or no awareness of the main issues in their industry — leaving them exposed as regulations increase, particularly around supply chains.

Companies operating in the EU would do well to prioritise supply chain management. Over three-quarters of companies have not integrated responsible procurement into their sustainability strategy. Adoption of the Corporate Sustainability Due Diligence Directive (CSDDD) will require mandatory human rights and environmental due diligence across the supply chain for large organisations from 2027.

In 2024, addressing employee engagement and wellbeing was also confirmed to make good business sense. Over 80% of executives believe that stronger commitments on employee rights would help them attract high-quality talent, appeal to new customers and increase profitability.

This comes as US companies roll back their diversity programmes. Issues including burnout, rapid skills development and adapting to the gig economy have been found to negatively impact the wellbeing of almost half of workers globally.

Discussion of human rights was never far from the headlines in 2024. The European Parliament gave final approval to the Forced Labour Regulation banning the import and sale of products suspected to be made using forced labour. In the UK, a landmark ruling relating to the import of cotton from China put increased pressure on the National Crime Agency to investigate allegations of supply chain mismanagement. Meanwhile, concerns emerged about the human rights record of COP29 host country Azerbaijan.

Top tips to prepare for the year ahead

Map your value chain and assess risks. It is essential to understand your company’s actual and potential social impacts and put in place plans to address them.

Publish commitments. As regulation increases, companies face growing pressure for transparency about their impact, but many are failing to be open about their human sustainability goals.

Publicly report impacts and due diligence processes. CSDDD requires companies to produce an annual statement on its potential and actual adverse impacts and due diligence measures.

05. Sustainability leads challenged by reporting

Sustainability leaders became increasingly concerned about the reporting burden in 2024.

Over 70% of sustainability professionals indicated that a growing focus on reporting was taking them away from the real work of delivering their sustainability goals. It has proved a particular headache for companies facing reporting requirements across multiple jurisdictions. One in three companies also have sustainability goals due to expire in 2025. They need to carve out time alongside reporting to evaluate progress and reflect on future challenges with a view to setting new targets.

Complying with the Corporate Sustainability Reporting Directive (CSRD) topped the list of challenges. It became a reality for 12,000 companies in 2024. In June, the majority of sustainability professionals polled were confident that they would be ready by the year-end deadline. But relatively new requirements, such as disclosures on biodiversity, circularity and workers in the supply chain, were proving challenging.

All eyes will be on this first wave of reports in 2025 and the extent to which their reports are deemed compliant. Watching particularly closely are the large private companies that need to prepare for their first mandatory sustainability report in 2025.

Despite long being an advocate for more reporting, there were signs of a slowdown in Europe, as 17 Member States failed to ratify the CSRD by the September deadline. This led to baby steps towards a simplified reporting regime consolidating multiple requirements — a new Omnibus Simplification Package is due out in February 2025.

Outside Europe, mandatory reporting is on the rise, with new rules taking effect in India, Singapore and Hong Kong. Canada and UAE announced plans to make reporting compulsory for larger organisations. The UK progressed with endorsement of the IFRS Sustainability Disclosure Standards — moving closer to adopting it as a successor to the Task Force on Climate-related Disclosures.

Top tips to prepare for the year ahead

Survey your sustainability universe. For those facing mandatory reporting for the first time, build a solid base by conducting a thorough double materiality assessment.

Update your strategy and targets. Based on the outcome of your materiality assessment, update targets to establish clear ambitions for 2026 and beyond.

Revisit your communications. With so many new regulations, it can be hard to know what good looks like. Review stakeholder needs and how you share your story with them, learning from peers — especially if they take a different approach.

Keep an eye to the future. Determining ‘materiality’ is challenging, but crucial as regulation increases. You may have to report a broader set of issues in future, especially as the Corporate Sustainability Due Diligence Directive approaches.

Supporting you in the year ahead

We can’t tell you exactly how things will play out in 2025, but we do know that there will be ever greater demand for action.

We’re helping clients to navigate the evolving sustainability landscape through strategy, reporting and communications support. If you’d like to chat about how we can help you prepare to face this and other challenges, please get in touch.

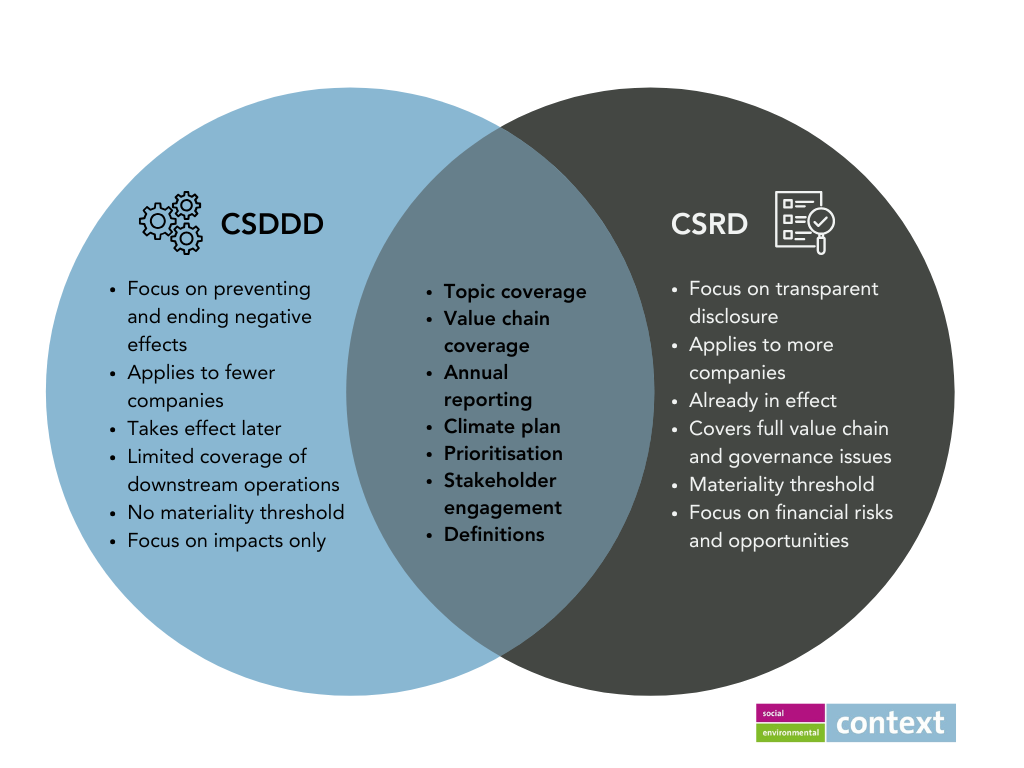

CSDDD is a due diligence legislation requiring companies to identify, prevent, reduce and end negative human rights and environmental impacts in their operations and value chains. Companies also need to report annually on impacts and actions. Read our blog on everything you need to know about CSDDD.

CSRD is a reporting directive requiring companies to perform a double materiality assessment and produce an annual report disclosing the impacts, risks, opportunities and action plans associated with their material environmental, social and governance (ESG) issues.

What are the key similarities and differences between CSDDD and CSRD?

Core focus

CSDDD focuses on doing — taking action to end adverse impacts. CSRD focuses on materiality andreporting — identifying and transparently disclosing impacts. But there is crossover. Like CSRD, CSDDD also requires annual reporting on adverse impacts and mitigation actions. And although CSRD is more focused on reporting than action, it does ask companies to disclose their climate plans in line with limiting global warming to 1.5°C.

Scope and timeline

Both apply to large companies operating in the EU. CSRD applies to more companies, including EU-listed SMEs, and is already in effect. CSDDD is narrower — only large companies with 1,000+ employees and a net turnover of €450+ million are in scope. Companies must comply with CSDDD by 2027 at the earliest.

Topic coverage

The topics covered by the legislations are broadly aligned. Both include human rights and environmental impacts and acknowledge their deeply interconnected nature. CSRD has the bigger picture in mind, covering issues related to governance, consumers and end-users. It also focuses on financial risks and opportunities, unlike CSDDD.

Value chain coverage

Both cover companies’ own operations as well as upstream and downstream operations — inside and outside Europe. But CSDDD has a smaller downstream scope, only covering certain operations such as distribution, transport and storage. CSRD goes further and covers end-users and product disposal.

Climate plans and reporting

Both ask for a climate transition plan aligned with limiting global warming to 1.5°C, and a publicly available annual report covering impacts and actions. CSRD’s reporting scope is more ambitious — see topic coverage above.

Prioritisation

Both require companies to prioritise impacts based on severity and likelihood. But CSRD’s double materiality assessment means companies don’t have to report on issues that are less relevant to them. CSDDD still requires companies to address lower priority impacts after addressing their higher priority issues.

Stakeholder engagement

Organisations need to continuously engage with internal and external stakeholders for both legislations. CSRD adopters must engage with stakeholders to perform the double materiality assessment and gather the necessary data. CSDDD requires stakeholder engagement throughout the due diligence process — from strategy-setting and training to providing a complaints procedure and monitoring due diligence measures.

Targeted SME support

Unlike CSRD, CSDDD adopters must try to avoid overly burdening business partners who are small and medium-sized enterprise (SMEs). This could include offering training to SME suppliers or upgrading management systems, and where necessary providing financial support.

Definitions

The definitions of impacts, risks and opportunities are aligned across the legislations. Impacts refer to potential and actual effects organisations have on the environment and society. Risks and opportunities refer to how sustainability issues could affect the organisation’s balance sheet.

What’s left to do if you already report to CSRD?

If you’re already on top of CSRD then you’re covered for CSDDD reporting and climate plan requirements. But there are some due diligence measures you’ll still need to carry out for CSDDD:

Create a policy that ensures risk-based due diligence.

Carry out in-depth assessments of individual suppliers in prioritised areas.

Take measures to prevent and mitigate potential adverse impacts, and minimise and end actual adverse impacts.

Provide a notification channel and complaints procedure.

Monitor the effectiveness of due diligence measures and update them accordingly.

Provide targeted and proportionate support for business partners who are SMEs, including non-discriminatory contractual assurances.

Context is ready to support you with all your CSRD and CSDDD needs — from devising strategies and conducting double materiality assessments, to writing policies and reports. If you would like to talk about your organisation’s needs, please get in touch via www.contextsustainability.com or helen.fisher@contexteurope.com.

Companies currently reporting toward Sustainability Accounting Standard Board (SASB) or Taskforce for Climate-related Financial Disclosures (TCFD) will need to transition to the new International Financial Reporting Standards (IFRS) Sustainability Disclosure Standards for reporting years beginning on or after January 1, 2024.

Launched by the International Sustainability Standards Board (ISSB) in 2023, IFRS Sustainability Disclosure Standards (also known as the ISSB standards) provide investors with decision-useful, globally comparable sustainability-related information. Whether or not companies have previously reported to SASB and TCFD, those looking to voluntarily apply IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and S2 (Climate-related Disclosures) will benefit from a newly launched guide. It offers essential guidance as companies work toward full disclosure with the standard.

Our key takeaways from the guide include:

1. Voluntary application and investor expectations

IFRS S1 and IFRS S2 respond to investor need for transparent, comparable, and reliable data on climate and sustainability risks. While full compliance is encouraged, companies may implement the standards progressively. This flexibility allows companies to gradually build the necessary reporting systems and capabilities.

2. Clear communication on compliance

Companies will need to clarify the extent of their application by regularly updating and communicating their assessment of their progress toward compliance.

3. Transition reliefs and phased implementation

Recognizing that some companies may require time to converge on full disclosure, the ISSB has introduced transition reliefs. For example, companies may focus on climate-related disclosures in the first reporting year, with broader sustainability disclosures phased in later. Additionally, although IFRS S1 requires sustainability-related financial disclosures to be reported simultaneously with financial statements for the same period, companies may delay reporting sustainability information alongside financial statements and may defer certain disclosures, such as Scope 3 greenhouse gas emissions[i].

4. Proportionality mechanisms

To address varying levels of readiness, the ISSB has included proportionality mechanisms. These allow companies to report using “reasonable and supportable” data available at the time, without incurring excessive costs or efforts. Companies can apply qualitative approaches where quantitative data may be difficult to obtain initially, which is particularly helpful for first-time reporters or those with limited resources.

As companies transition to the ISSB standards, it’s important to note that many jurisdictions worldwide are either considering or have already mandated sustainability reporting aligned – either closely or partially – with the ISSB standards. At the time of this posting, jurisdictions that have adopted ISSB-aligned disclosure regulations include Bangladesh, Brazil, Costa Rica, Turkey, and Nigeria. Other jurisdictions such as New Zealand and the United Kingdom have adopted climate-related disclosure standards based on the TCFD recommendations. The UK government has also announced plans to create UK sustainability disclosure standards based on the ISSB standards.

No matter where you’re at in your disclosure journey Context can help. Whether its pulling together your first IFRS index, disclosing to CSRD, or creating a sustainability report that your stakeholders want to read, we can support you. Please reach out to myself (kyisin.aung@contextamerica.com) if you’d like to discuss your organization’s needs.

[i] Although the ISSB offers transition relief on Scope 3 emissions, California has enacted a new law (Senate Bill 219) requiring businesses to disclosure their climate-related financial risks and carbon emissions, including Scope 3. For companies operating in California, analyzing Scope 3 emissions will be a priority.

Businesses have long recognised that they can and should make a meaningful contribution to the UN Sustainable Development Goals (SDGs). And there’s a big prize on offer for solving major economic, environmental and social challenges and delivering on the goals — an estimated $12 trillion in business opportunities.

But in a growing number of cases, alignment is superficial, leading to accusations of SDG-washing — using the SDGs as a way to imply greater social and environmental impact. For example, the company mentions that it is partnering to deliver the SDGs (goal 17) because it has joined an industry body aimed at tackling deforestation, inequality, or another recognised sustainability challenge. Yet, it has not made any changes to its current sustainability strategy or ways of working.

Here are Context’s top tips for using the SDGs to drive meaningful change within your business.

1. Create a detailed map to guide your journey

For each of the 17 high-level goals, there are up to 12 targets — 169 targets in total. And for each target, there are between two and four indicators of progress. But many companies don’t look beyond the headline goals.

A comprehensive approach to SDG mapping requires companies to assess both their positive and negative impacts at the target level. It enables you to understand where the organisation can have the biggest impact, but also identify the trade-offs — where pursuing benefits in one area could cause harm in another. Building a new coal-fired power station improves access to affordable energy (goal 7), but also generates increased emissions slowing climate action (goal 13). A thorough evaluation also ensures no opportunities or risks are overlooked.

You will need to look at many of the same sources you use to identify and assess your company’s sustainability matters as part of any Double Materiality Assessment. Combining the two provides a rounded view of the company’s impacts, risks and opportunities.

2. Explore the full value chain

SDG mapping should cover the full value chain — not just the company’s own operations. A pharmaceutical company’s core focus on improving health and wellbeing (goal 3) may be undermined if new treatments can’t get to market. Looking upstream and downstream helps to identify the areas where partnership is essential for delivering on the aims of the SDGs (goal 17).

3. Adopt a less is more approach

With the exception of some multinational, portfolio businesses, few organisations can have an impact on all 17 SDGs. It is better to focus on just a few core goals without becoming blinkered to the company’s impacts — positive and negative — on other SDGs.

If impact is genuinely broader than just a few goals, you could reference linked goals where company actions create co-benefits. For example, providing better nutrition (goal 2) may help children to concentrate better in schools and enjoy the benefits of quality education (goal 4).

Transparency breeds trust. Stakeholders expect a company to explain its approach to prioritising the SDGs. That means showing the company has selected the areas where it can make the biggest impact and directly contribute to the target. A record of providing employee training does not represent a contribution to quality education (goal 4), though improving access in emerging markets to the textbooks the company produces might.

It also means acknowledging that the company can’t have a positive impact in all areas — and indeed in furthering one goal may generate trade-offs in another area.

4. Mind the gap

Companies should focus on the SDGs where they can have the greatest impact. But less scrupulous organisations have adopted the same approach with dubious motives.

Consider the soft drinks company that focuses on sustainable consumption and production (goal 12), but fails to address (or even acknowledge) its impact on good health and wellbeing (goal 3). Or how about the fossil fuel company that focuses on decent work and economic growth (goal 8), but overlooks climate action (goal 13).

These are deliberate instances of SDG-washing. But companies can face similar accusations when they fail to explain why they have chosen to put the focus on some areas and not others.

5. Integrate the SDGs into the core business

Some companies pepper their annual sustainability report with logos of the individual SDGs, but then the goals are not mentioned again until the following report. True impact only stems from integrating the goals and targets within the business.

Researchers at Stanford University have identified companies that have embedded the SDGs into everything they do. African technology company Safaricom has woven the goals into its statement of purpose, descriptions of team tasks and even personal objectives. This helps to explain how the finance team provides ‘transparency and visibility on our procurement practices and fighting corruption in all its forms (goal 16)’ or HR promotes decent work and good labour practices (goal 8).

Meanwhile, Danish biotechnology company Novozyme uses the SDGs as a lens to decide which new products to advance and which to shelve.

6. Measure and demonstrate progress

Impact is hard to measure, particularly in relation to systemic issues. Over 80% of business leaders have indicated that measurement challenges prevent progress towards the goals.

This is where comprehensive SDG mapping comes into its own. The Stanford researchers highlighted how Ramboll assessed revenues against its priority SDGs to identify which business units directly contributed to delivery of the goals and which didn’t. By shifting focus on to the business units with greatest impact, it was able to demonstrate progress towards the goals, while reducing negative impacts elsewhere.

7. Approach the SDGs as you would other reporting frameworks

Most companies mention their contribution to the SDGs in their annual sustainability reports, but rarely treat disclosures with the same level of thoroughness as other reporting frameworks such as the Global Reporting Initiative (GRI) or the IFRS’s International Sustainability Standards.

Greater visibility is needed. If a company says it is contributing to the SDGs, its commitment and actions should be clearly connected to the SDGs targets — and supported by robust data. The GRI’s business reporting database provides guidance on how the SDGs align with common reporting frameworks, enabling the SDGs to be integrated into wider reporting activities. Done well, it reassures stakeholders that companies are serious about their social and environmental impact and build trusts.

Referencing the company’s contribution to the SDGs in the CEO’s introduction to the annual sustainability report demonstrates that the commitment comes from the top of the organisation.

Context supports companies to map their impacts and understand their contribution to the SDGs and their material issues. This provides the foundation for robust sustainability strategy, reporting and communications – beyond the addition of a few SDG logos to your report. If you would like to talk about your organisation’s needs, please get in touch via www.contextsustainability.com or helen.fisher@contexteurope.com.